From ICO to ILAO: The Evolution

ICO stands for initial coin offering. The first ICO occurred in 2013. You must have heard something about it. But did you know that the ICO market is one of the most successful in terms of business loans?

That the ICO market has risen and fallen like a phoenix?

That there are numerous names in the ICO industry…

Don’t worry if you can’t answer every question. Now, let’s discuss each in greater depth.

History and mythology

Myth is a sort of cognition of reality that serves to capture reality’s most significant parts through representations that are basic and easy to understand. For example, a river represents the boundary between life and death, and Hercules is the archetype of a hero..

Myths, on the other hand, can be very negative. “ICO is a complete scam,” one of them says. It was created by well-known media, but nearly no one bothered to investigate it after that. In addition to DAO Synergis and other enthusiast teams. And after more investigation, it was discovered that everything is not so awful, or rather, everything is just fine: the degree of scam in the ICO market is lower than in bank financing to enterprises, and even lower in the VC segment: approximately 16 percent versus 25–33 percent.

You’ve undoubtedly heard of Ethereum (2014), Tezos (2016), Bancor (2016), Chronobank (2016), Waves (2016), Tron (2017), Brave (2017), Cosmos (2017), Polkadot (2017), Filecoin (2017), and more cryptocurrencies. All of these are huge and successful ICOs.

And the third thesis, which debunks a widespread misunderstanding, is that ICO goes by several names: let us try to grasp them while also tracing the growth of the phenomenon.

From ICO to ILAO

Let’s take a quick look back.:

Crowdfunding surfaced as a method for gathering investments without the assistance of institutional investors, however after raising funds, enterprises attempted not to repay monies to investors due to at an early stage of the project, investors did not have formal confirmation of participation.

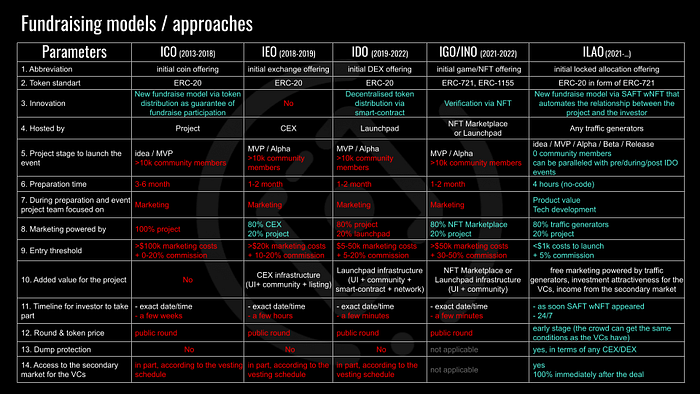

ICO provided contributors with the chance to obtain a coin or token in exchange for contributions that serve as proof of the contributor’s involvement in a specific project. But this sort of appeal did not instantly take off due to the caliber of the projects and the level of expertise among crowd investors..

IEO was advertised to the market as a sort of solution involving professional project verification by centralized exchanges, but it did not see much development: to some extent, the bear market did not have it, and it was also not a core area for the exchanges themselves, but only one of the channels for luring new projects for listing (although BNB is just the colossus of that era).

With the development of DEXs, IDOs and fresh market players emerged as go-betweens between the project and the crowd investor, called launchpads. Their job was to thoroughly assess ideas, assist with marketing and KOLs, and publish the project on DEXs following the initial token sale.

With the introduction of ILAO, projects now have a 24/7 opportunity to communicate directly with investors without the use of middlemen; all that is required to verify the value hypothesis is an MVP and a basic community. Additionally, aggregators can now replace launch pads where projects will attempt to obtain and maintain information about projects that is as relevant and appealing to investors as possible. Previously, aggregators stood aside and primarily monetized through advertising and referral links. But DEXs, CEXs, lunchboxes, and other players can’t just stand by..

Now, in order to better appreciate the usefulness of ILAO, let’s enumerate the ICO rebirths, specifically:

- ICO — Because nobody understood tokenization in 2013, the phrase “initial coin offering” (ICO) was created..

- ITO — Initial token offering already refers especially to a derivative entity, i.e., a token that, unlike a coin, is already formed on another party’s blockchain and is derived from the currency itself (for instance, an ERC-20 token to ETH);

- TGE — an effort to avoid drawing comparisons to initial public offerings (IPOs), which are risky because to SEC persecution about the Howey test and other peculiarities, and instead refers to token generate events.

- STO — Security token offering is the term used by the SEC and those who want the “fastest integration” of the venture capital and Web 3.0 worlds, but the hype hasn’t materialized in 6 years because of the high entrance barrier and stringent regulation.

- IEO — Later (in 2019), major exchanges joined the ICO, and thus the Initial exchange offering was born.

- IDO — In 2020, DEX offerings (including launchpads) decisively won the race, hence the name was changed to Initial DEX offering..

In the meantime, other acronyms have always denoted the initial placement of crypto-assets and the gathering of payments on them for the project. Here are several examples:

- WHO: Wallet Holder Offering — initial offer to wallet owners.

- IFO: Initial Farm Offering — Initial Farming offering

- OPT: OpenPredict — predictive models for derivatives and other insurance instruments that may have an initial offering;

- ILP: Initial Placement Loan — A loan for an initial placement: an operation to purchase tokens after identification, where the token acts as a (investment) loan for the project’s development.

- SCI: Safe Coin Investments and here — citation “Safe crypto-currency venture capital investments in diverse business enterprises. The annual percentage yield (APY) is utilized to finance projects, as stipulated by SCI smart contracts.”

- IGO: Initial game offering — became popular in 2021 as a result of the introduction of the GameFi sector.

- INO: Initial (w)NFT offering — also rose to prominence in 2020–2022 due to the NFT craze in GameFi, Metaverses, digital art, and a great deal more. According to us, one of the most promising areas being implemented is DAO ENVELOP comprising SAFT and additional micro DAOs

- IAO: Initial airdrop offering is a collective phrase including multiple token accumulation mechanisms for active action service users. Examples include ENS, 1inch, Uniswap, ShapeShift, Optimism, etc. (also see references: 1, 2, 3);

- IDaO: The initial DAO offering will be discussed later, as DAOs have only gained momentum since 2016;

- ILAO:Initial Lock Allocation Offering… and more about it below. And yes, not to be confused with ILOs — Initial Liquidity Offerings nor Initial Listing Offerings.

ILAO. Details

ILAO (Initial Locked Allocation Offering) — solution for crowd and/or institutional investors.

In this case, it’s crucial to start with the project-related principles that were in place prior to the ILAO. Almost the same set of responsibilities were included in all actions linked to bringing the project to any of the ICO-like events:

- Start with an alpha or minimal MVP version of your product.

- Whitepaper, tokenomics, pitch deck, onepager, website.

- Attract the first private (at least) or venture capitalist (preferably) investors.

- Create a community — here, channels and methods change every 3–6 months with the market: for example, in 2017, it was viable to “pour” visitors through Google or Facebook, but in 2021, AMA sessions and KOLs were effective.

- Negotiate with Launchpad/s, whose market was built and changed by the hype of IDO trends (DeFi->Art NFT->GameFi/Metaverse (play2earn/move2earn…

- Develop a CEX/DEX listing plan.

- Find and select MarketMaker, as well as accept the risks linked with the transfer of funds to management (at least for CEXs).

All these complex tasks, except for developing an actual product, require the bulk of the time and resources of the project.

Imagine the efficiency and speed of product creation if projects didn’t have to decide where to conduct IDO and which MM to shift to liquidity management. These efforts made sense until a technology arose that could secure the safe distribution of tokens for the project before listing on CEX/DEX and without the need to implement marketing, launchpads, and listing.

Everything changed in the spring of 2021 when the DAO ENVELOP team introduced the idea of “time-lock” (also known as “vesting period”), which gave the market the opportunity to wrap project tokens in wNFT with a variety of smart settings to ensure that all functionality is closed within a wNFT.

As a result of these features, DAO ENVELOP team tried out ILAO on themselves and distributed NIFTSY tokens on their own wNFT for the first time via the wNFT Launchpad (then it was called that) just prior to the main IDO in October of 2021.” At the same time, the ENVELOP team and Tier-1 VC Animoca Brands made history by partnering with SAFT wNFT for the first time.

Research revealed that there were many more benefits of SAFT wNFT and ILAO as a new ICO format than were initially apparent at first glance.:

Following customer development with several dozen VCs, it was discovered that 23 of predominantly medium VCs, who typically invest in 70–150 projects per year and up to $70M each, confirmed their interest in using SAFT wNFT in their activities with an assessment of readiness to increase investments (frequency and volume) up to 50% — in other words, projects that communicate with VC and are ready to ship their tokens in the form of SAFT wNFT increase the chance of success.

Consider the traditional methods of token distribution: 1) manual sending by projects and/or 2) branding of tokens by funds from “scanners.” In either case, the fund must wait until the conclusion of the subsequent vesting term before receiving access to the eagerly expected tokens. The second strategy is creating a unique smart contract, more commonly referred to as a “locker,” to which a pool of project tokens is deposited, vesting schedules are established, and a white list of fund addresses is developed, for which tokens will be unlocked in accordance. Solidity’s Middle/Senior developers spend 2–4 weeks creating a smart contract of this caliber, which has a $4–7k market value. If the project has the necessary skills, the cost will range from $2 to 3.5k. And that’s the bare minimum.

For example, SAFT wNFT’s subscription fee is only 200,000 NIFTSY tokens, which are returned to users in the form of wNFT after a year-long time-lock. This means that SAFT wNFT is only available for a month under the terms of the deposit of the NIFTSY token, where a derivative backed by the same tokens is available. This can be relatively painless for users..

The user can immediately sell wNFT with locked NIFTSY tokens inside after subscribing. Users who opt to keep their wNFT tokens will be able to deploy them and withdraw previously locked NIFTSY tokens after 12 months to use for new subscriptions, staking, or to sell on CEX/DEX if they like.

NFT tokens issued to contributors as wNFT minimize the possibility of them being dumped on the CEx or DEX as they can only be exchanged on NFT marketplaces or OTC platforms..

Timelock is only one of many smart settings that make SAFT wNFT use cases more reasonable for projects because it is based on the ENVELOP protocol. Other smart settings include profiting from secondary market resales, which enables projects to benefit from the speculation market even when prices are falling. It is difficult to deploy wNFT and level all accessible parameters prior to the Timelock before which it is impossible.

Let’s give an example: The project and VC agreed on a 100k USDT investment, and VC verified its long-term objectives during the negotiations. VC requested that he be sent 100 SAFT wNFT with project tokens worth $1,000 apiece, even though the project, for example, has ten vesting periods, for the sake of expediency. An optional commission of 500 USDT is established for each transfer of 100 SAFT wNFT from one wallet to another, and a 100 percent royalty is set for the transfer of all 100 SAFT wNFT VC that are generated as a result. In order to sell SAFT wNFT before the vesting period, VC must have 500 USDT on the wallet to perform the transfer operation. This means that for a sale that is not below cost, VC will have to sell at a price of 1,500 USDT at least for each of 100 SAFT wNFT, the second buyer (VC or crowd investor), for resale to zero, will have to set the price at 2'000 USDT, and so on. It doesn’t matter what the VC chooses, the project will receive an additional $500 USDT from each resale. The project receives an economic MM if VC sells at or above zero, resulting in a profit for the project and a rise in the secondary OTC market price of the project token.

LAUNCHPAD KILLER?

The VC community driving audience should also be taken into account; some investors join syndicates in order to acquire huge allocations on the best conditions from projects. With SAFT wNFT, the project may connect with these investors in a secure manner, release its tokens in greater quantities than the typical Launchpad ticket (200–500 USDT), and quickly draw in new contributors.

The product turned out to be so convenient that the DAO ENVELOP team decided to give access to it to every user and now this service is available in a few clicks — yes, yes, you were right: in a few minutes you can issue wNFTs containing any ERC / BEP-20 tokens, with established vesting periods (aka Time-locks) and offer them to contributors by direct transfer or through a specialized OTC Engine Tool — SCOTCH.

This is also where the abbreviation ILAO comes from: Initial Locked Allocated Offering — as an initial offer of locked tokens inside wNFT or SAFT wNFT.

What does this mean and how will the life of projects change with the advent of ILAO?

- Teams can now concentrate more on generating the final product rather than promoting it.

- Less time will be required to test the hypothesis of the project product’s value; projects will be able to implement MVP and immediately offer the market to participate in the project, thereby collecting feedback from the community, ready to “vote with a coin” for the project idea at any time, without incurring marketing costs.

- The focus of projects will shift from launchpads to information and analytical resources that bring together large numbers of users who look at the project market for “instant” investments without waiting for a specific IDO date, which is what happens now on launchpads.

- The risks of sniping bots will decrease, respectively, there will also be fewer companies offering anti-sniping bots -> the market will receive new decentralized tokens.

- Profit from resales in the secondary market may exceed the volume of attracted investments for popular projects.

- Conducting an ILAO in terms of resources will be comparable to conducting a custom development.

- Many infrastructure projects will appear around and based on SAFT wNFT.

Results

Therefore, regardless of what the media and various analytical agencies from earlier eras claim, it is quite obvious that ICO not only hasn’t died as a phenomenon, but has also evolved and received many incarnations. This means that Web 3.0 markets will continue to develop further as people begin to put openness, anonymity, and decentralization into practice, and DAO ENVELOP will contribute to this by developing more and more new tools for startups in this amazing, complex industry.