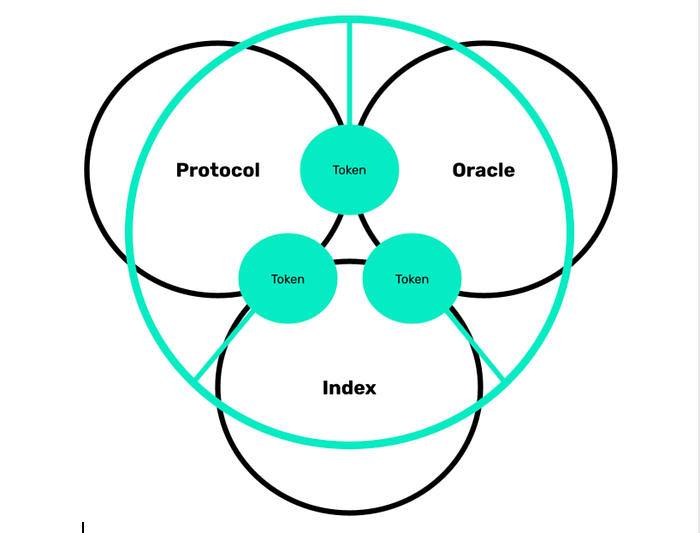

Protocol. Oracle. Index. Token. Or why NIFTSY is not afraid

Before working with a project, I always ask it questions and see whether the team understands the risks of the market or whether all it possesses is rabid optimism. No, I am not against optimism, but without racy epithets, because there was not much scam in the ICO, let’s say, but it is remembered precisely because there was a lot of objective, where young and not so “optimists” did not take into account the clear demands of the market.

So, below is the NIFTSY risk hedging model, where on the one hand it presents market analysis of contingent competitors (I don’t believe in competition of p2p startups due to the principle of self-investment) and on the other hand it describes scaling of their monetization model. Simply put: it presents the architecture of the project in broad strokes.

Through the oracle to the truth

So, let’s repeat: NIFTSY Protocol — formalization of all those operations you can perform with NFT (issuance, wrap/unwrap, royalty payments, recurrence payments to the collateral, etc.). Oracle is a decentralized system for assessing risks associated with NFT of any order (level), which includes a scoring system, classical ant-fraud and AI-anti-fraud. The difference of the latter from the classic one is the following: a) heuristic analysis model, b) almost complete automation of decision making, c) possibility of data-mining (finding previously unaccounted correlations). Finally, the Index — formalizes the market as a whole.

But why do we need such a structure? Yes, and a Token to it as well. Well, let’s figure it out.

In fact, at each level we offer the same thing — insurance against total ruin:

- At the Protocol level, it serves as a pledged, replenishable vault (the same Collateral), which in no way can burn out unless the market collapses or was originally formed as a set of fake tokens. But… in the latter case there is Oracle.

- Oracle also insures against collapse, but not of one or a set of assets wrapped in NFT, but of what will fall, as they say in the market, “will bounce”, some startup: firstly, the assets are scoring, that is you can evaluate risk before buying (on 100-point scale), secondly, at the moment of buying/holding/selling the assets get scoring from anti-fraud system. And even if you bought an NFT with a collateral vault where some of the risky assets are pledged, when they are completely zeroed out — some part of the vault will still remain.

- But what to do when the whole market collapses? We need a stablecoin, but not tied to the fiat price or to the commodity price (gold, silver, real estate, etc.), but created by the market itself. And in NIFTSY this is the Index.

Now a little more detail about each element. In terms of cursory market analysis: read the general one in our first article, i.e. the link: https://niftsy.medium.com/nfts-market-meta-analysis-by-niftsy-e9f131234041.

Protocol

If something can be repeated, it can be unrepeated: in the sense that the uniqueness of a product is always greater (and higher) than the sum of its elements. Here are some examples:

- https://charged.fi/ — a protocol recently completed by IDO and successfully (for which we congratulate him), according to the documentation: “With the Charged Particles Protocol, you’re able to turn ANY NFT into a DeFi NFT. It’s still that NFT, e.g. digital art piece, you know and love — but now it’s able to have an actual underlying intrinsic value and accrue interest over time.” (in NIFTSY — more familiar: Collateral), programmable interest.

- https://nftx.org is another project close to ours in a number of aspects, where the documentation, again, gives all the answers: “Users deposit their NFTs in an NFTX vault and mine a replaceable ERC-20 token (vToken), which is a claim on a random asset from the vault. The vTokens can also be used to redeem a particular NFT from the vault… Simply put, collectors can use NFTX to get more value from their NFTs: Earn a commission for the protocol (coming soon); Earn a commission for trading as a liquidity provider, etc. Content creators launching NFTX can earn protocol commissions indefinitely, as well as improve reach and distribution fairness; Earn protocol commissions; Distribute NFT through AMMs in the form of vTokens; Create instantly liquid markets for new content. Finally, Investors can, as NFTs are not usually (yet) very illiquid and difficult to price, NFTX makes speculation and investment in the NFT market a much easier process, for example through access to the most liquid NFT markets or by tracking the price of certain NFT categories.”

- https://burnt.com is the latest example, which is interesting not only because it has attracted $3m investment from Alameda Research and other crypto funds, but also because it is built on a blockchain… Solana. Again — go to the documentation and see: “Burnt Finance is a fully decentralized auction protocol built on Solana. Burnt Finance is a DeFi protocol that enables anyone to mint a diverse array of synthetics and NFTs while also providing them with an unparalleled auction platform. Burnt is powered by the Burnt Token (BURNT) which handles governance procedures while also offering fee reductions on the platform for new creators”.

Shall we compare? Yes, and we get the following:

- Not only the three protocols described, but all the others that are close to them (and to us), that were analysed earlier, contain one but crucial mistake: the creators somehow think that the price in the market is determined solely by fairness. Unfortunately, this is not true: selling blanks is an everyday practice and not only (and not even so much) in the p2p market. And it can only be solved if: a) on the one hand, the process of issuing and other NFT transactions is formalised (this is the Protocol’s responsibility); b) on the other hand, it has internal, onchain, and external, off-chain, value verification parameters (Oracle is responsible for this).

- Minting is a popular and interesting process, but in fact neither it nor any other operation of interest accrual and/or creation of some entities at the expense of collateral (storage) of others is possible if there is no understanding of working with liquidity of the second and subsequent levels, especially if such is wrapped just in NFT, which has its own internal, dynamic Collateral. That is, minting cannot be the primary and/or primary operation of the Protocol. Simplifying: it is difficult (if not impossible) to create something secured on something that may not itself be secured.

- And while all the protocols are similar, there is still a significant difference between what underlies them: the key difference of NIFTSY is that it is a “pure protocol”, meaning that the use of a token in it is completely secondary. Why? We’ll tell you about that below.

In the meantime, let’s move on to the second part — Oracle.

Oracle

First of all, it is worth noting that the first oracle hype took place and was quite successful and immediately there was a clear gradation of them:

What should be called classic oracles:

- https://chain.link — a project that links smart contracts to the outside world.

- etc.

The next category is market analysers:

- https://www.chainalytics.com — perhaps the best known of them all.

- https://crystalblockchain.com is the second number one.

- https://glassnode.com is also a well-known project in this field.

- Here, too, we can gradate by blockchain, for example: https://www.nansen.ai — gives out those very “signals” on Ether.

The largest category, perhaps, is aggregators of two types:

- https://analytics.skew.com/dashboard/bitcoin-spot — which collects data from various open sources and from market analysts.

- And it is information aggregators, which are also divided into two types:

General — where the best known is CMC:

- https://coinmarketcap.com/nft/collections/

- https://www.coingecko.com/nft and its permanent competitor

- Specialized:

- Say, https://dappradar.com

- However, the list is easily continued.

A separate type should include analytics services that provide frequent or ad hoc information about the crypto market and its segments, including NFT:

- https://www.statista.com is one possible example.

- PWC and others from the big four, etc.

And now one question remains, “then why is it Oracle NIFTSY?”. It’s simple if you look closely at the proposed classification and identify the errors of existing solutions. Here they are:

- As soon as the Oracle depends on one token, the latter inevitably starts to rise in price and this causes excessive speculation and manipulation in the market. But in the end, this approach distorts the market, which should be objectively valued.

- The situation becomes even worse if data analysis is purchased as a pricing plan, as ChainAnalitics has, for example: there is no question of openness and decentralisation. If we remember the manipulation of the markets in 2005–2007 and in 2018–2021, and the creation of fake agencies like Diar, it turns out that centralisation is not achieved by the data itself, it is distributed, but in the process of adding value to it (it becomes information).

- Finally, it all boils down to the fact that the data from the market and the aggregators of information can diverge, and sometimes significantly. Beginning with trivial failures (https://twitter.com/CoinMarketCap/status/1404380113383432194) up to premeditated distortions. And as a result, those, who must earn on fair play (exchanges, exchangers, media and others) — go to the dark side of the Force and overstate the volume of trades, manipulate the price of tokens, etc.

- At the same time, there are already (partially) implemented ideas for integrating different data into a single stream:

- https://thegraph.com — directly on the market.

- https://nftndx.io — through verification of NFT actors’ personalities.

In our view there is an adequate response to this:

- Oracle should NOT be directly dependent on the project token.

- Oracle should be decentralised;

- Oracle should give data to any member of the network on request: what exactly will pay for the request is a secondary question.

The data itself should not be stored inside a blockchain — bundles like the ones created by Synpat, where data is placed as magnet-links in torrents, IPFS hashes, as well as storages like Chia or Filecoin, or in blockchains, but working with data.

Otherwise, Oracle is supposed to be a set of publicly available and open smart contracts that will eventually spawn another brainchild of the project, Index.

Index

Index represents the last DAO (see last section for more details) of those that can operate separately from a DAO with a NIFTSY token. The Index has four hypostases:

- Serves as a hedging tool to the whole NFT market at once (“pure” NFT, wrapped, derivatives of different order, liquidity wrapped in NFT, digital art objects in the form of NFT and so on): by buying share in DAO, you buy a kind of shard/part of shard insurance, which is akin to buying share in DPoS-systems, but only in this case you enter not in project but in NFT-market in general.

- It helps Oracle to evaluate any project: let’s say you want to produce electric cars today. Can a luxury one cost $10,000? No? Then the only segment such a project could occupy is countries like India, where a plywood “car” could cost as much as $1000-$3000. Simply put, you take an NFT startup of any format. At any level. At any stage.

- Creates a tool for selling the whole market at once: it depends not only on the primitive price of each NFT-token, but also on total turnover (transactions), number of users and other on- and off-chain (thanks to Oracle) metrics.

- It develops more and more methods of formalisation behind the Protocol (more on that later).

And this DAO already has its contingent competitors:

- https://nftindex.tech — “a digital asset index designed to track token performance in the NFT industry… Always less volatile than more concentrated portfolios. Fall protection due to a wider selection of tokens”. But there are problems: a) valuation is done again via USD; b) the token is fixed to the Ethereum market; c) has a limited set of valuation categories (directions).

- https://www.piedao.org — with roughly the same problems of platform and project anchoring.

And it is the Index that sees all the pluses of NIFTSY:

- Crosschain — we don’t create bridges or set up gateways between different blockchains (although we can use Polkadot, Cosmos, Avalanche and other solutions), but we help work with any NFT of any order (level) in any blockchain and/or other decentralised and/or distributed system (graphs of various kinds, say). More on this below: in the Token section. Already today we are working with EVM-compatible platforms, next up are Solana, Cardano and multi-blockchains.

- We don’t have a focus on the top 10, top 30 or top 100 projects — all of this does not unify, but rather differentiates markets. We take any entities that can be unified with the Protocol and verified with Oracle and put them into the Index, and the Index itself is built on the principles of decentralisation and openness (self-regulation).

- And yes, the NIFTSY Index is also a DAO, so anyone can become part of it. And it does not necessarily have to be an entity.

But how are all three elements connected? Through the fourth, the Token.

Tokenomics, or the Token as a Binding Element

I first encountered tokenomics in 2014: when the Ethereum ICO took place. And since then I have gone over this topic both inside and out: I even published a book on Web 3.0 and tokenization together with E. Romanenko. But the question still raises a pleasant surprise. Why? Because there is a lot of innovation in it.

So, in NIFTSY I decided to advise the team on a scheme, what is called “growing up”:

- Each element (Protocol, Oracle, Index) can be used separately and you don’t have to pay for some interesting features via NIFTSY Token.

- But if you want to get a “turnkey solution” or use some combination of, say: Protocol + Oracle, Oracle + Index, or even Protocol + Oracle + Index, then you can’t do without Token. In fact, he, the Token, plays the role of technical, binding element — the glue, which lets each of the DAO (and all three listed elements — DAO), that now they need to work together and provide the client with the most complete picture of the NFT-world and/or its segment.

- You will also need a Token if you suddenly want to be part of a meta-DAO: not just part of a Protocol, Oracle or Index, not only to manage processes through the Token, but also to develop the NIFTSY community (it’s built on the basis of a decentralized autonomous organization, after all).

This is what makes NIFTSY different from many other projects. Let’s go over it again and from a different angle:

- You can directly issue, store and otherwise circulate funds by communicating through NFT entities of any order. Through Protocol.

- You can do it either through Oracle or any other third party, or generally through pure p2p relationships.

- You are always the direct owner of the assets, if they have been wrapped through the Protocol, for example.

- But you can go further and enter the market as a whole — through the Index, hedging yourself against the strongest fluctuations inherent in many micro projects.

- In doing so, you can use both the API layer and smart contracts to customise your own based on the existing bundle (Protocol + Oracle + Index).

- Role assignment helps to solve the storage problem as well (you can also explore the addressing problem, which is solved by multi-chain storage bundle on one side, and by Oracle and Protocol working together on the other side): “If an NFT is to retain its value, it has to be stored somewhere — if all copies are deleted, then there’s nothing to own! This requires us to take a number of issues into consideration, ranging from who should be responsible for storage, to the desired levels of redundancy, accessibility, and longevity of the data being stored”.

- And yes, this approach makes tokenomics what it should be: flexible.

Why flexible? I’ll answer in more detail in another study, but here are just a few important points:

- Firstly, the crypto market in 2011 and 2021 are two different markets and while BTC was first a means to play and donate, then a means to make payments, today it is the best hedging instrument in the world. So why shouldn’t the Token expand its functionality?

- Secondly, the flexibility of multiple DAOs makes it possible to develop each element separately or together with others, which in turn allows to modify the Token’s functionality. And the Token is announced as a cross-chain…

- Third, and it is the cross-chain property that helps us conduct one, extremely simple, but also very important operation: we can create NFT of any order with collateral storage in any blockchain and by “freezing” it, transfer all those assets to another blockchain, where NFT is created via Protocol. Without complicated setup and other operations. Or with them: it depends more on the final decision of the parties

As of today, the Token has the following declared features therefore:

- Ability to integrate Index, Oracle and Index into different subsystems.

- The ability to activate special features of the Protocol (Oracle, Index), such as:

- Dynamic Accumulation;

- Royalty payment to authors;

- Adjustment of recurrent payments in the accumulator;

- Minting and more.

- In this case Token is initially created in ERC-20 standard, and then issued of any blockchain if necessary and subject to freezing of initial Token in liquidity funds (read more in article about Tokenomics).

And that’s what we end up with — a generic DAO NIFTSY scheme

If you are interested, stay in touch with us:

- https://t.me/niftsy_en

- https://twitter.com/niftsyprotocol

- https://www.youtube.com/channel/UC7LIhhtsKhb3sFGGs43chMQ

And to!